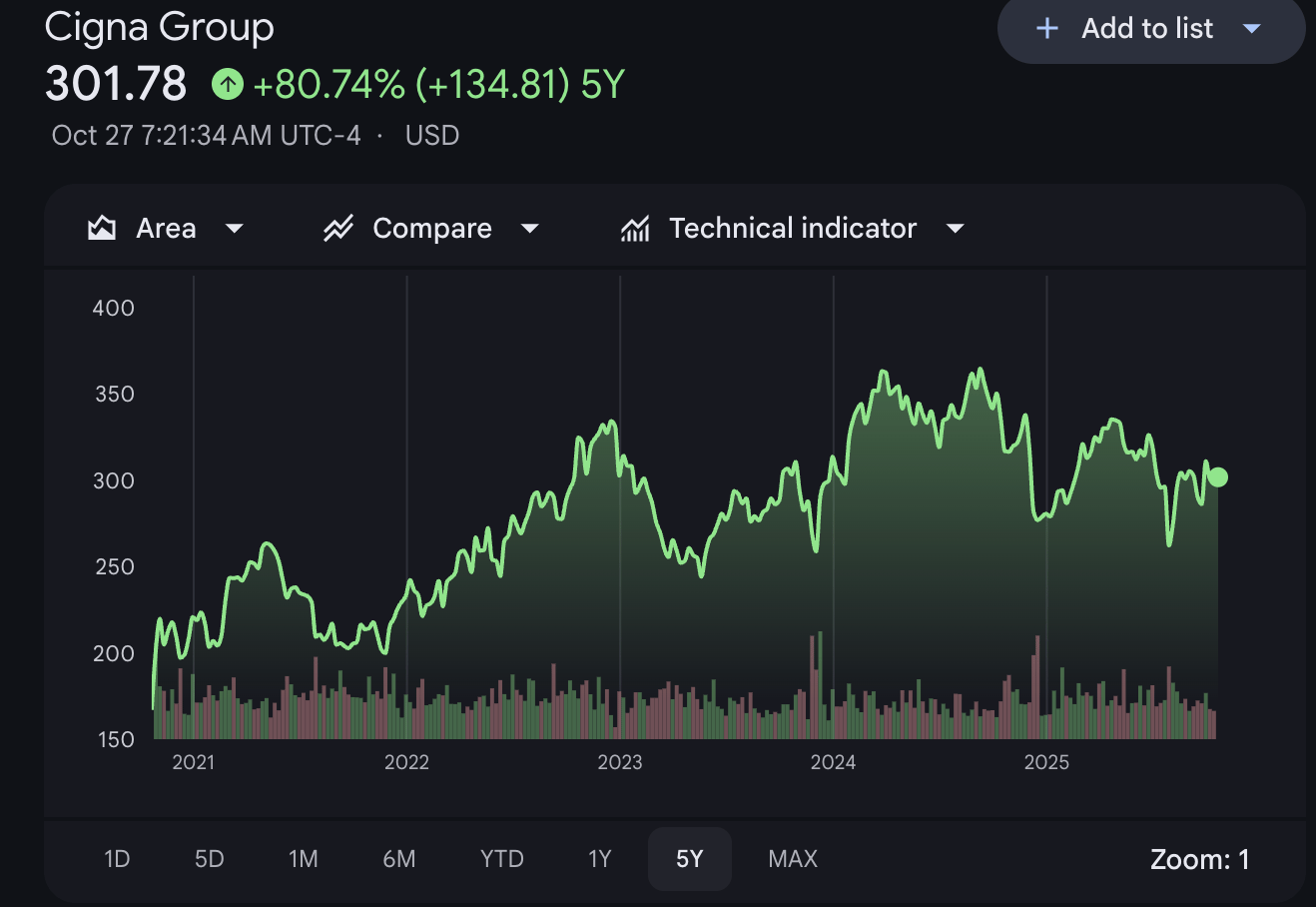

How Cigna keeps beating the odds

Special thanks to our friends at Aequitas Partners, the sponsors of this post.

Aequitas Partners, a firm that builds leadership teams for high-growth healthcare companies, is running its 6th Annual Healthcare Executive Compensation Survey. Over the years, this study has become the seminal reference for CEOs, executives, and investors as they grow their teams. If you participate, you'll receive the benchmarks (base, bonus, equity) by function, level, and company stage - completely free and exclusive to the healthcare industry.

PARTICIPATE IN THE SURVEY HERE.

(Extended deadline is November 7th, with results sent only to participants in December.)

Today, Cigna took a preemptive step in the conversation around reforming pharmacy benefits by announcing it will end drug rebates across many health plans by 2027. Its stock took a dip in the hours following the news, before rebounding. What’s unclear is how significant this move will be in the federal government’s agenda to bring more transparency to drug pricing. Overall though, the company is a standout in its peer group for having a generally good run over the past few years. So I’ve spent the past few months talking to the industry - current and former employees, analysts, researchers and bankers to figure out why.

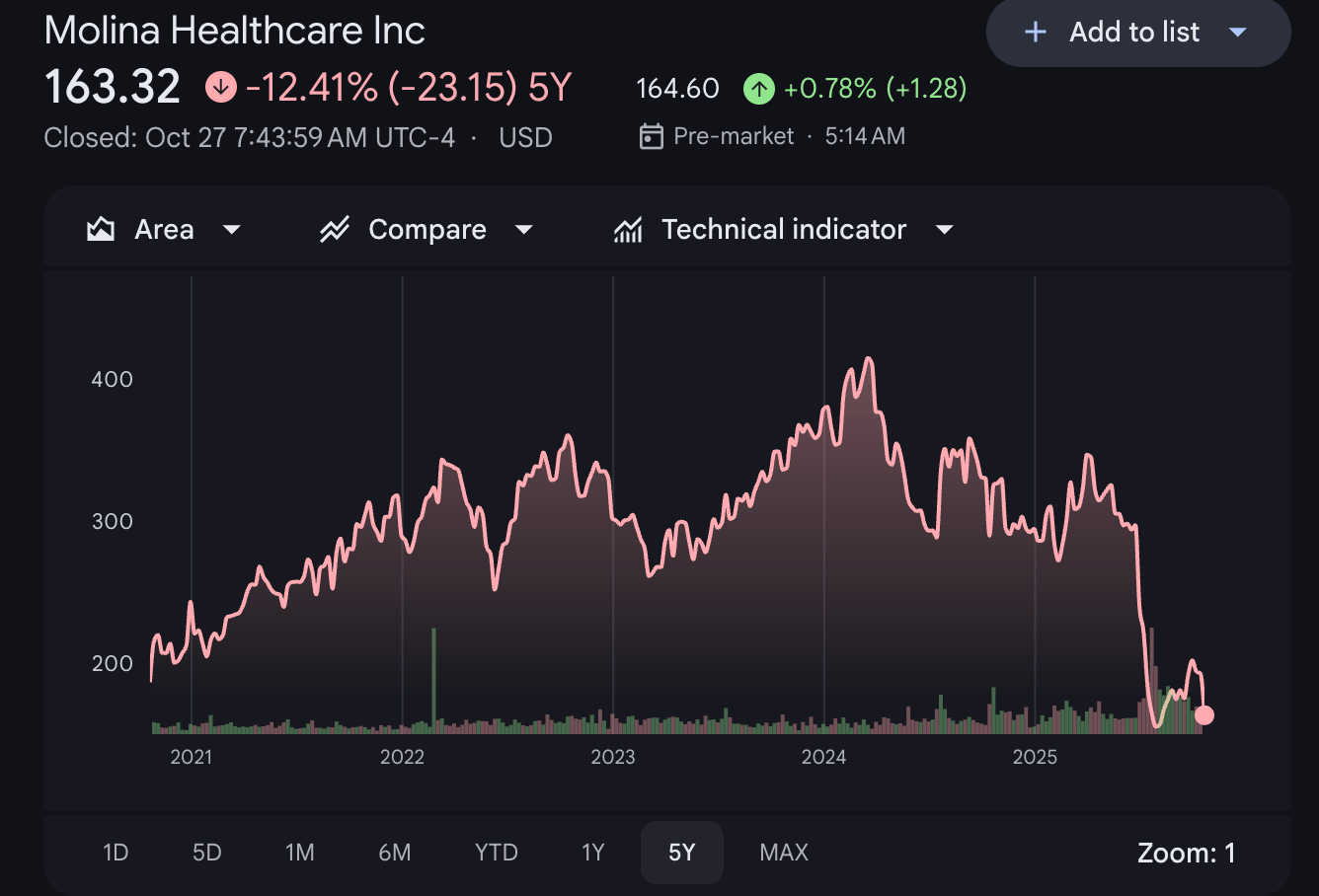

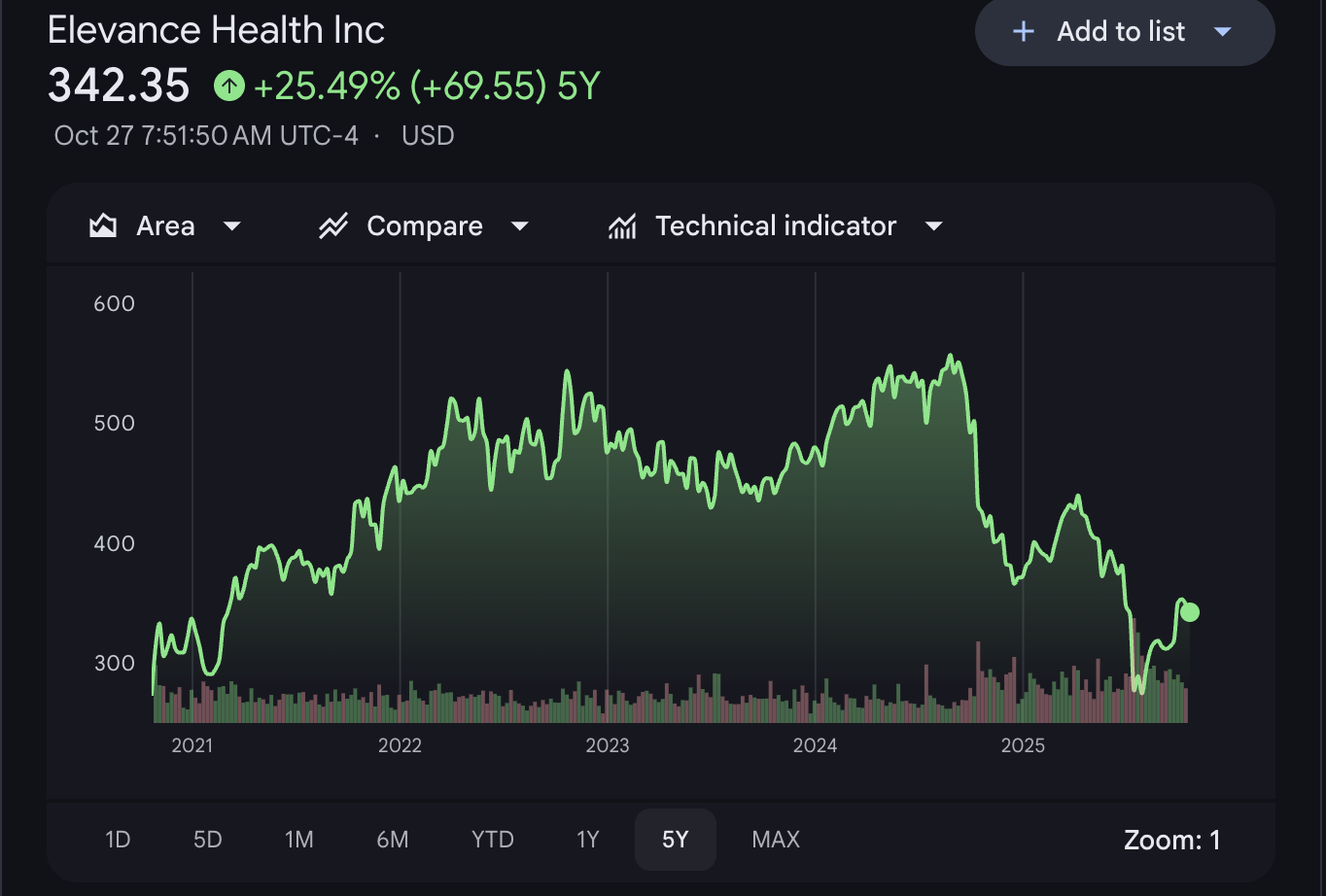

Cigna hasn’t escaped rising healthcare costs. But its performance continues to meet (and sometimes exceed) investor expectations, buoyed by multiple quarters of strong earnings and several years of steady growth. Compared to peers like United Healthcare, Humana, Centene and Aetna, Cigna’s stock performance has been remarkably resilient.

As one former health plan executive put it:

“They were either very smart, or very lucky, or both. They zigged when everyone else zagged.”

Cigna’s success has a lot to do with timing, focus, and disciplined strategy…particularly its decision to step away from government-sponsored plans at just the right moment. So let’s talk about it, and why it matters to our industry.

Why Cigna’s business mix works

Cigna’s peers dove deep into Medicare Advantage and Medicaid expansion, while Cigna remained more tethered to the commercial health insurance market. Some analysts once viewed that as a weakness, as fewer government contracts meant less guaranteed growth. But in hindsight, that conservative positioning has worked in its favor.

Cigna also owns one of the “big three” pharmacy benefit managers (PBMs), through its Evernorth division. While PBMs face growing calls for reform and transparency around drug pricing, Cigna’s integrated structure gives it scale, cost control, and leverage across its health services portfolio.

As one former executive put it:

“If it wasn’t palatable with the Street, we listened.”

Leaving Medicare Advantage behind

While Medicare Advantage (MA) remains a lucrative but volatile space, it’s risky. Utilization is rising, reimbursement cuts loom, and administrative burdens continue to grow. Meanwhile, players in the space are struggling to keep costs down due to social determinants of health for their members (lack of housing, quality food, transportation and so on) and are struggling to maintain star ratings.

When it set out to win market share in MA, Cigna struggled to gain ground against major players like UnitedHealthcare and regional Blues plans. So, earlier this year, it made a decisive move: selling its Medicare Advantage business to Health Care Service Corp. (HCSC) for $3.3 billion.

That sale removed a drag on profitability and freed up cash (and mindshare) to focus on its commercial strengths.

“Getting out of the government business is the main reason it’s outperformed its peers for the past 18 months,” one longtime Cigna insider said.

“Cigna seems to have realized that if it couldn’t compete they would start to see an inevitable fall in the market when there are too many competitors and a diminishing share,” added Christopher Kerns, the CEO and cofounder of Union Healthcare Insight, a research firm focused on the healthcare industry.

Doubling down on Evernorth and specialty pharmacy

Cigna’s biggest bright spot is its Evernorth segment, especially Accredo, its specialty pharmacy arm. Specialty medications are one of the fastest-growing sectors in healthcare, treating complex and chronic conditions like cancer and autoimmune diseases.

Cigna recently invested $3.5 billion in Shields Health, a specialty pharmacy company formerly owned by Walgreens. CEO David Cordani described the deal as part of a long-term bet on the rapid expansion of specialty care.

Specialty pharmacies don’t just drive revenue; they cement relationships with patients and employers. With new therapeutics and precision treatments entering the market, this is the growth engine to watch.

Winning the commercial market

Cigna’s other edge lies in its commercial health plan offerings, particularly Cigna Level Funding. This “bridge” product serves employers with 50–1,000 employees who are too large for fully insured plans but not ready for full self-insurance.

Level funding lets employers pay predictable monthly rates while gaining more control over claims and costs. It’s become one of Cigna’s most successful innovations, attracting venture-backed digital health companies and mid-sized employers alike. There are copycats in the market, but few players that have pulled off level funding as profitably as Cigna.

“It turned into a very attractive product in the market,” one digital health executive said.

That segment isn’t just high margin; it’s strategically sticky. Once employers are onboard, Cigna can layer in other high-value services, like oncology care management or pharmacy optimization. It also has a strong relationship with the diabetes-focused care management company Omada Health, which also sells into employers and health plans.

Culture and leadership: Cigna’s quiet advantage

The digital health community tends to view Cigna positively in part due to its leadership stability. CEO David Cordani is often described as a thoughtful, strategic executive who retains talent and builds loyal teams. People who succeed at Cigna will ascend up the ranks, and stick around for long stints. There’s less of a “churn and burn” culture, versus other health plans, which I’ve heard consistently makes the company easier to work with for digital health companies.

The company’s Chief Health Officer, Dr. David Brailer, has helped steer Cigna toward being more patient-centric, even tying executive compensation to customer satisfaction. And Cigna’s relatively “asset-light” model also helps. Unlike some peers with sprawling clinic networks and retail operations (think UnitedHealthcare’s Optum or CVS Health’s MinuteClinics), Cigna remains focused on scalable, lower-capital business lines.

The other benefit to Cigna's size, versus say a behemoth like United Healthcare, is that the company isn't so large that it can only grow through acquisition. With too much M&A, it’s very challenging to create an integrated culture, noted Kerns, the healthcare researcher.

What’s next: more M&A?

Don’t rule out future deals. Cigna has cash, credibility, and ambition, and analysts are whispering behind closed doors about potential M&A activity. To be clear: I don’t have any inside knowledge, but it wouldn’t surprise me (or any of my banker friends) if Cigna revisits talks with Humana. With the sub-scale Medicare Advantage business now divested, antitrust scrutiny would likely be far less intense and a mega merger possible. If a move like that happened, it would likely occur in the near-term (2026 or 2027) while Cigna is well positioned to do so - meaning before the inevitable MA rebound.

The company could also seek partnerships with Centene or other payers to expand its footprint in targeted markets. An acquisition of a player like Centene might be on the table, also, but seems less likely than Humana given its large presence in MA. Healthcare is cyclical — and Cigna will be actively thinking about how to ride the next wave.

MA will more than likely come back. Baby boomers will continue to turn 65 and go on Medicare, and there’s a market that is still continuing to choose it. Those who have a strong business in MA can make real margins and the market has historically rewarded that. It’s hard to imagine there will be additional MA cuts. Commercial rates are already so much higher than Medicare that it’s hard to imagine that happening anytime soon.

The bottom line

In a brutal season for health insurance stocks, Cigna stands out as a rare example of steady performance and strategic restraint. By focusing on commercial markets, specialty pharmacy growth, and a disciplined M&A strategy, it avoided the worst pitfalls that caught competitors off guard.

For now, if you have to be a health plan, you’d probably want to be Cigna.

Want more analyses like this?

We regularly profile healthcare companies, from legacy payers to emerging startups, to unpack strategy, leadership, and market dynamics.

Know a company you’d like us to feature next? Hit reply or drop a note.

About the author

Christina Farr

Christina Farr is a healthcare writer and investor. Formerly at CNBC and Reuters, she covers digital health, startups, and policy, blending reporting with analysis and investing perspective to help leaders navigate healthcare’s evolving landscape.

New York City