A top healthcare VC ponders whether there will be another value-based care home run

Thank you to B Capital’s Adam Seabrook for saying the quiet part out loud. We talk ad nauseam about value-based care at events and conferences, but the fee-for-service payment model continues to dominate. Most of us agree that value-based care is where healthcare should be going in the future, but progress has been slow because it’s easier said than done. It’s my personal view that until we can put pen to paper and explore what is required to invest in value-based care – longer timelines, heavier capital requirements, and so on – then the opportunity won’t get the allocation it deserves. And Adam has done that, while honestly asking the question of whether venture investors can make Power Law returns by investing in value-based care.

As a follow-up to this column, I’ve invited Adam and a panel of experts to join me on a LinkedIn Live to discuss venture capital and value-based care, as well as alternative funding sources. Stay tuned!

By Adam Seabrook

The U.S. health insurance industry has been working on transferring financial risk to providers for at least two decades, even as progress has been slow1. The goal of all of this change is to better align provider incentives with the health outcomes of the patients they serve. If fee-for-service (FFS) entices providers to do as many exams and procedures as possible to maximize revenue, then value-based care (VBC) flips that incentive by encouraging providers to control the cost of care through a share of the profits derived from treating a population of patients efficiently. There’s more to gain than just affordability; there’s the potential to offer higher-quality care, as well as services that are not traditionally billable in a fee-for-service construct.

Analyzing the Trailblazers in VBC

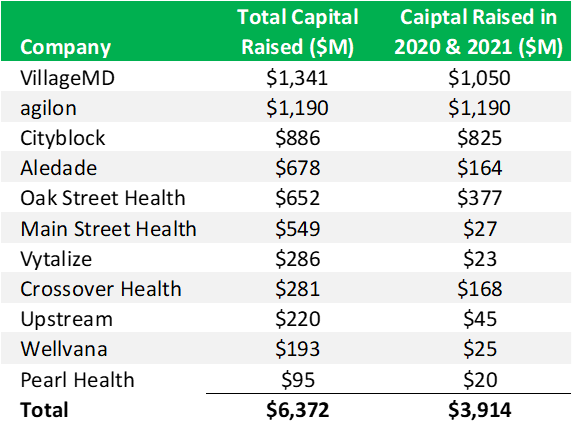

For investors, it sounds like a lucrative opportunity and the proposition has attracted billions of dollars of venture and growth capital. Let’s take a snapshot of the largest companies in the value-based care arena, and the capital they’ve accumulated to date:

$6.5B is a lot of money and it’s interesting to see that more than 60% of it was raised in 2020 and 2021 when the Fed funds rate was effectively 0%. Capital was certainly more freely available. After all of that investment, it’s worth asking the question about whether or not VBC is a good place to make an early-stage investment. While the opportunity may sound incredibly attractive, and there’s no doubt VBC is moving healthcare in the right direction, it remains a big challenge for investors to see a return on their investment commensurate with the risk they take.

I’ve studied VBC business models for years, and here’s my thesis on it: The form of VBC with the greatest potential upside, and therefore the largest incentive for providers to change the way they practice, is global capitation - a fixed per member per month (PMPM) payment model for which the recipient is required to cover all of a patient’s expenses but also gets to capture any potential savings (see this great article on the 2024 results for MSSP, which is another alternative payment program that many providers join in lieu of taking full risk on patients). Oak Street Health, ChenMed, and Iora Health are all examples of companies that provide(d) primary care in exchange for payments under global capitation.

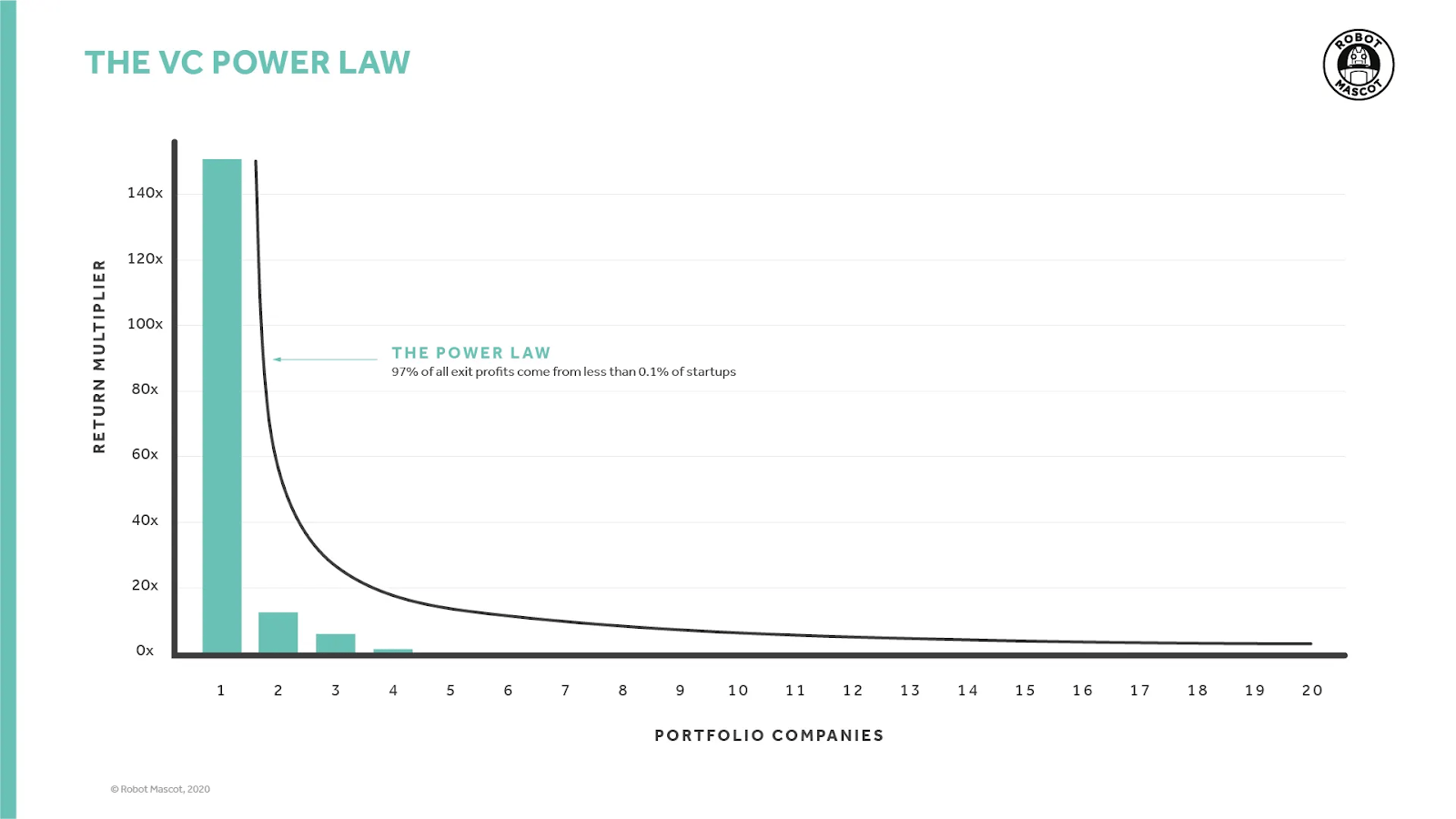

As an investor, it’s an interesting place to look for ROI because if you lower costs, which so many companies purport to do, then you get paid better. Unfortunately, there isn’t a great deal of returns data available for these companies, but Oak Street Health (now owned by CVS) can serve as an illustrative example. By all accounts, the company was a success story when it went public and then was acquired for $10.6B. That makes it one of the largest acquisitions in the category to date. But looking at the math, would early stage investors make the same decision again knowing the risk/reward tradeoff? Does it fit the power law2 thesis of venture capital, that espouses the idea that if an investment doesn’t have the potential to make 100x the initial investment then it probably doesn’t make sense for the earliest stages of venture capital?

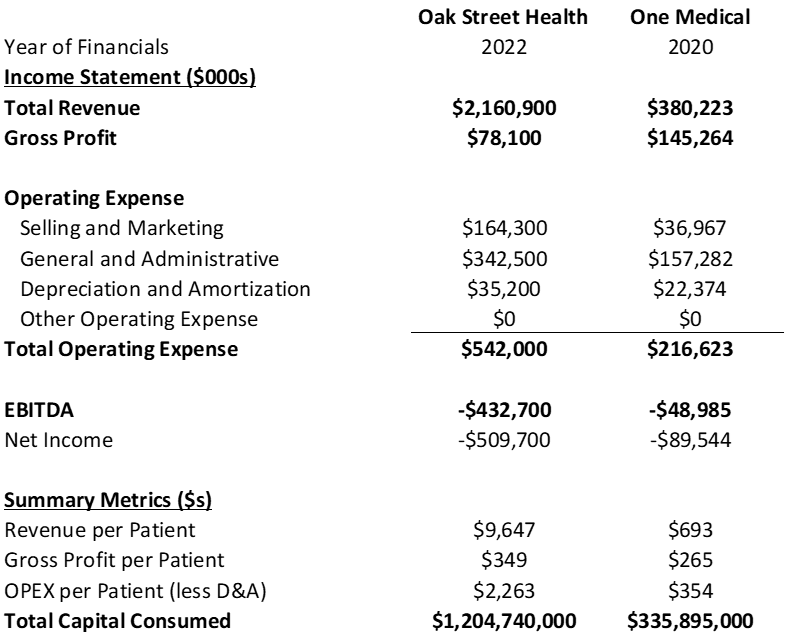

Let’s break it down. How did the earliest investors in Oak Street Health do? Oak Street’s earliest round of funding came from Oxeon (the health-tech recruiting firm) and TLSG (an early-stage fund). Per PitchBook, these funds only invested in the Series A round prior to the IPO, which makes it easier to calculate their returns. These two firms owned a combined 879,844 shares before the IPO3, which were worth a total of $40.2M based on the $10.6B acquisition price (if they held onto their shares). We don’t know exactly how large the Series A was and we don’t know if either firm sold any secondary shares between their original investment and the IPO, but we can make some estimates. First, the company was founded in 2012 and PitchBook data shows that the average early stage deal size in 2012 was $5.8M. That’s a 6.9×4 return on the original investment. That’s a significant outcome for a fund but it’s not the kind of fund returner that the Power Law chart suggests one would need for a home run. Would the first institutional investors take the same risk again when presented with the knowledge that the company would raise and consume $1.2B in equity and debt in order to get to an exit at a multiple of 4.9x gross revenue while still losing $500M per year? I can’t answer that, but one way to reframe the question would be to ask whether you would invest in a VBC company compared to a similar company with a FFS business model, knowing what we know now about VBC. Oak Street and One Medical, a predominantly FFS business, are compared in the following table/figure.

One Medical (now owned by Amazon) was much closer to profitability, consumed less capital to get to break-even (nearly 75% less), had a higher gross margin, and lower OPEX per patient. Again, I believe in the mission of VBC. But when you look at the outcomes it’s hard to argue that VBC has been a better financial investment than FFS. I’d love to be proven wrong on this, so if anyone has a different analysis to share, my inbox is always open.

So where have I landed on all this?

Although VBC may not be an attractive investment area as it stands, it’s still the best set of incentives we’ve got to get providers to focus on lowering the cost of care. So what needs to change in order to make it work for venture investors, knowing their job is to return capital? The most obvious place to look would be the operating expenses (OPEX), meaning the indirect expenses necessary to run a business that are not associated directly with providing care. The operational complexity in running a VBC business is always going to be higher than it is for a comparable FFS business. For example, a new VBC company has to build or acquire clinics, develop and implement a patient acquisition strategy and a member engagement program that allows them to serve attributed members proactively. A FFS company, in comparison, can take any member from any insurer and is typically much more reactive in their engagement with patients (i.e., they see them when they call for an appointment). In the case of One Medical, in addition to the direct-to-consumer sales channel they also go direct-to-employer, which can help lower customer acquisition cost. Not unexpectedly, Oak Street’s sales and marketing expense was 210% of gross profit while One Medical’s was only 25%.

VBC companies also need to build a data set and analytics capability to understand underlying health conditions, prioritize patients, find the correct contact info, acquire ADT (admissions-discharges-transfers) feeds from hospitals and HIEs (health information exchange) to manage transitions of care, and other insights necessary to control the cost of care. FFS companies need none of that. Unsurprisingly, general and administrative expenses (i.e., non-clinician salaries, office rent expense, R&D, etc.) for Oak Street were 439% of gross profit while One Medical spent 108% of gross profit. VBC care models simply require more operational overhead to do well than FFS care models.

“There are deeper reasons why OPEX was so challenging in what I think of as VBC 1.0,” said Catherine Olexa-Meadors, Head of Growth and Partnerships at Town Hall Ventures, who spent the last 12 years in leadership roles at VBC companies Aledade and Remedy Partners (now Signify Health). Patient engagement and acquisition aligned with risk contracts was “uncharted territory,” she explained.

Early players like Oak Street Health had to secure payer contracts and capitated risk, identify where patients were, build physical sites, and recruit patients—all while running a complex, high-cost care model. Data and interoperability gaps compounded the challenge, forcing companies to create tech-enabled workflows and patient prioritization tools from scratch.

“These companies were sorting through dated payer reports, messy claims, and disparate EHR, ADT, and pharmacy data—trying to meet quality metrics, improve diagnosis coding, and drive preventative care,” Olexa-Meadors added. “For those who took risk, but didn’t enter into full capitation, historically fee-for-service clinics had to staff VBC engagement work and carve out time for proactive and transitional care visits, despite already feeling maxed out on bandwidth.”

In total, Oak Street’s OPEX per patient was more than 6 times greater than its gross profit per patient at $2,263. Part of that can be attributed to the expense associated with building new clinics and adding new patients, meaning the OPEX would be naturally higher than gross profit (this is the Oak Street Health J-Curve). At maturity, gross profit should be 3-5x the OPEX, but that is only possible through scale. There are many reasons why Oak Street’s OPEX is higher than it would be if it were a FFS business, but even as a VBC company - in my opinion - the ratio is not sustainable and needs to decline. The company’s OPEX scaled pretty linearly with revenue from 2018 to 2022, but they were projecting to get better leverage in 2023 and beyond:

The projection for 2025 roughly cuts OPEX per patient in half, but that would still mean OPEX per patient is nearly 400% of the gross profit per patient from 2022. Simply put, cutting OPEX just isn’t enough to get to profitability or to make the investment more compelling than a similar company operating under a FFS model. The only way for VBC to be profitable enough to outperform FFS is to drive down the medical loss ratio (MLR). That makes sense because many things you can do in VBC to reduce OPEX you can also do in a similar FFS company and there will always be operational complexities to VBC that do not exist in FFS so OPEX will be higher. MLR is also the place where the VBC business model has an advantage over FFS - if you find ways to use less care or reduce the unit cost then you get to capture the savings. Cost control takes time to improve, and is multifactorial. More mature cohorts should have better cost control performance.

The Oak Street coverage models I’ve seen from banks assume declining medical loss ratios over time, but the company wasn’t projecting to reach EBITDA profitability until 2026. MLR needs to go down faster. It’s well known that cost control takes time, is multi-factorial, and more mature cohorts should have better cost control performance. Because of this, impact on MLR may be uneven, and sometimes could be obscured when looking at all the clinics as a whole.

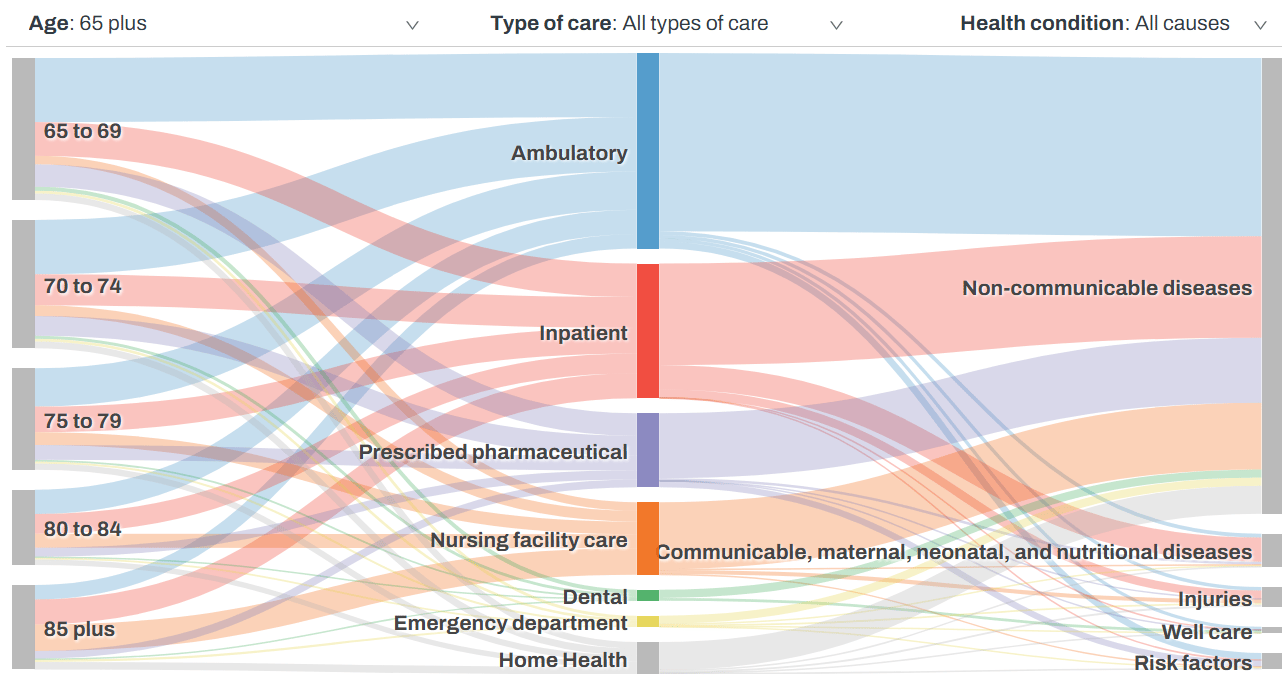

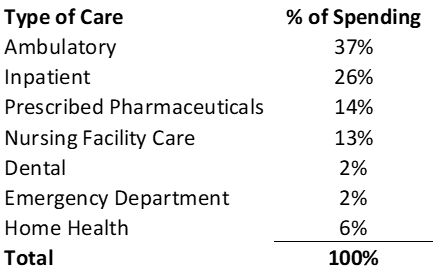

The chart below shows where the U.S. spends on patients 65 and older5:

And this is the breakdown in percentages:

There are certain costs any VBC company would be hard-pressed to affect. For example, the pricing associated with prescribed pharmaceuticals (although there is an impact when patients are prescribed generics versus specialty meds, whenever possible). However, between ambulatory, inpatient, and nursing facility care, the treatment of non-communicable diseases makes up 65% of the total cost of care for patients6. That’s an area where the cost of care can be affected through monitoring, engagement, behavior change, and a host of other factors. What kind of total cost of care reduction is necessary to make a meaningful impact on EBITDA? Below is a historical snapshot of Oak Street with projections from 2023 to 2025 from one investment bank’s coverage model:

If you could wave a magic wand and reduce the total cost of care by a desired percentage, here’s how those reductions would be reflected in Oak Street’s EBITDA:

By reducing the total cost of care by 15%, Oak Street could have been EBITDA positive in 2023 with no changes to their projected OPEX and they would hit >10% EBITDA margins in 2025. If they’d been able to implement the savings in 2018 the capital requirement would have been reduced by $760M. This type of EBITDA margin and reduced capital intensity makes VBC a much more interesting investment area. So, is it enough savings to make it more compelling for investment than investing in FFS? I think it’s the right order of magnitude. The high end of healthcare delivery trades at ~10x EBITDA. Even at 15x EBITDA, a 50% premium, the 2025 EBITDA with an additional 15% savings on total cost of care would yield a $9.1B enterprise value for Oak Street, about 10% below where CVS acquired the company.

Incremental Change is Not Enough to Power the Next Wave of VBC

How you generate those savings remains a huge question. Today, VBC exists most prevalently under Medicare Advantage plans. Optum analyzed claims data for members in VBC and FFS care models and found that the primary driver of cost savings were reducing hospital admissions and emergency department visits7. A similar Humana study found that VBC care models outperformed FFS care models on preventative care and chronic care management quality measures8. Those are great steps in the right direction, but even with these preventative steps most patients will still require care. ED visits, for example, only account for 2.1% of spending on patients over 659, so the impact on total cost of care is small even if all unnecessary ED visits are eliminated. VBC requires a new wave of innovation if we ever hope to generate the kind of savings described above.

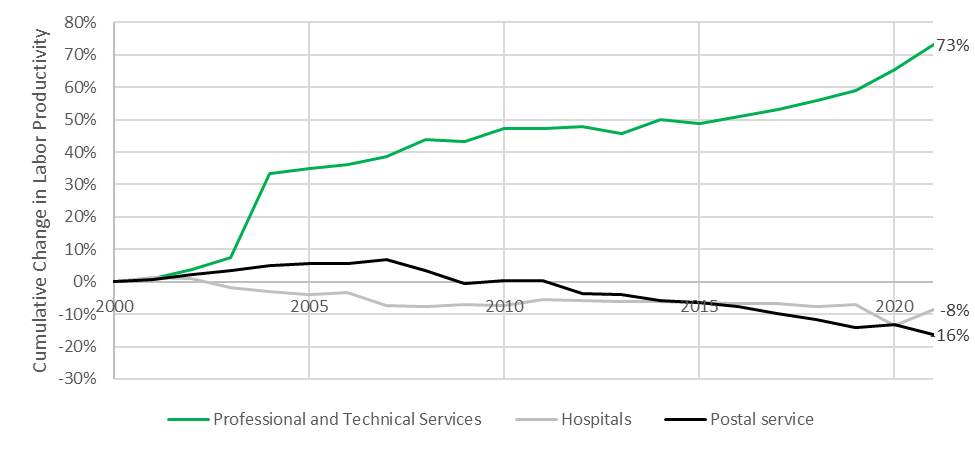

The coverage model the above analysis is based on already assumes that mature patient cohorts have MLRs of 75%. Lowering the total cost of care by 15% would require MLRs to be ~60% for mature cohorts. That is extremely low. Too low, I would argue, in today’s treatment paradigm. Productivity in healthcare has declined over the last two decades while productivity in other sectors has increased10:

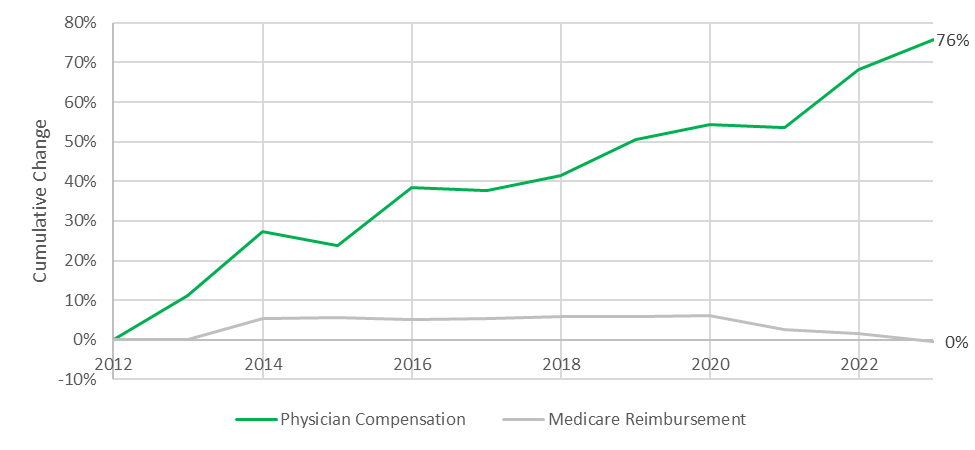

And physician compensation has risen even while Medicare’s reimbursement rates have remained flat11,12:

There’s no indication that we can make traditional providers cost-effective enough to get to 60% MLRs, which means early stage VBC, at least in its original form, won’t be more attractive than FFS as a venture investment in 2025. If there’s no investment in driving down cost of care, which FFS doesn’t incentivize, then we won’t be able to slow or reverse the runaway growth in the cost of healthcare in the U.S..

Everything I’ve just described is representative of the first wave of VBC companies - the trailblazers. It was important for the healthcare ecosystem that an enormous amount of capital flowed into the sector, and there were both winners and losers in the first wave. The question is not whether those were good deals to do at the time, but whether healthcare investors will continue to invest in VBC if we don’t make significant changes. If VBC companies take in huge sums of capital to build but don’t represent an attractive risk-adjusted return for investors, they are not going to be the solution to the United States’ healthcare cost problem. So do we allow healthcare to continue to grow at 5% annually until it swallows the U.S. economy or do we find another path?

What the Next Iteration of VBC Could Look Like

Fortunately, we’re at the very beginning of integrating AI into healthcare, which will revolutionize how our health system works. It’s starting with the administrative tasks like note taking, revenue cycle management, and call centers. These applications are great and will lower OPEX, but anything a VBC company can do in this arena a FFS company can do as well. To lower healthcare costs, and to make VBC a compelling early stage investment, AI must be applied to care delivery, and patient engagement is also a key frontier.

AI won’t reduce the total cost of care by 15% in one fell swoop. It won’t be applied in just one area. There are at least three buckets:

Non-clinical or administrative workflows - automated coding, claims denial management, patient steerage, etc.

Non-clinical tools with clinical and business impact - scribes, patient engagement and adherence, higher throughput without more CapEx, etc.

AI care delivery - therapy, specialty care, diagnostics, surgery, etc.

Category number 1 is obvious and category number 3 is where the market will eventually get to, but it will take time to become ubiquitous. Category number 2 is interesting to me in this climate because these solutions can expand provider capacity by increasing the amount of time clinicians spend with patients or increasing the throughput without significant new capital expenditures. Healthcare, and VBC, needs all three categories to have any chance of reducing the $5.3T the U.S. spent on healthcare in 2024. And it’s essential to make OPEX significantly more efficient (see the Oak Street example above) and find ways to decrease the cost of serving every type of patient encounter.

AI discovery company Perplexity estimates that about one third of a Medicare claim is the professional fee paid to the physician. A simple average of the RVUs (the units by which Medicare pays for healthcare) by CPT code puts it at about 50%. Based on that range, and because provider labor is only a portion of the cost of care: To save 15% in total cost of care, a company would have to cut physician utilization by 30%-45%. Some things, like ED care, may never be replaced so there would need to be deeper cuts than 30%-45% in other areas.

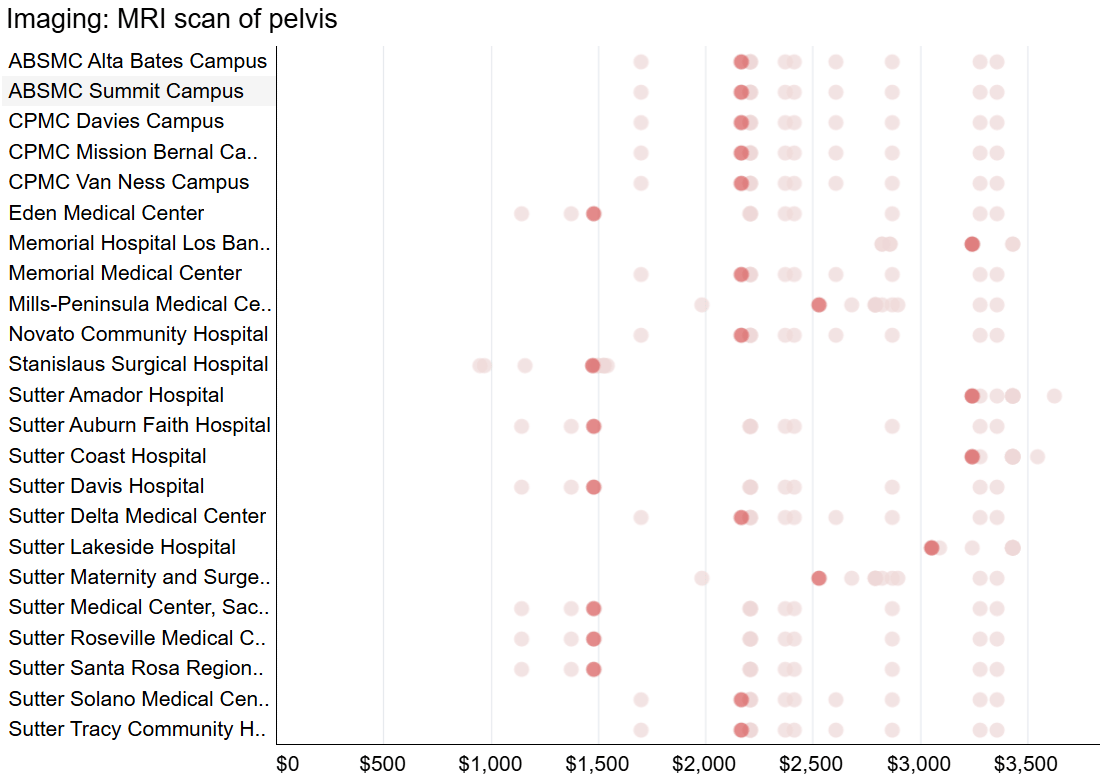

If you’re a founder running a VBC company, you’ll have to do things like refer patients for imaging and then convince the imaging center to let you interpret the images (via AI) yourself. The physician labor of an MRI of the pelvis, however, only accounts for 19% of the cost. That’s not enough, but if you owned the imaging center you could find savings by using AI to reduce the amount of time necessary to capture an image and reduce the number of views, which will let you get to the same diagnosis with less imaging time.

If you don’t own the imaging center, you have to reduce the cost of more intensive facility-based care. There are massive price discrepancies between facilities for the same insurer. Under a single commercial plan, the price of the same MRI of the pelvis may vary from $1,475 to $3,24413:

If the midpoint of cost is $2,360 and you select the $1,475 option, you’ve saved 37%. Add in the 19% savings from removing provider labor and you’ve saved 56%, on average. Fortunately, physician labor for specialty consults is typically responsible for 50% or more of the cost, so in some cases eliminating physician time is sufficient to exceed the 30%-45% range. For visits where the cost is almost entirely from physician time, like primary care and behavioral health, you need to eliminate nearly all of the clinical labor in order to help balance the inability to save on procedures and some diagnostic testing.

For procedures, like spinal fusion, prices range from $63k to $73k for the same commercial insurer:

If the midpoint of cost is $68k then you only save 7% by selecting the lowest cost site of care. Today, it’s harder to see where you can cut the physician labor from a procedure like this so, again, you need greater savings than 45% in other specialties or we need AI-enabled robotic surgeons.

To capitalize on the above price discrepancies, you’d need the data to create a narrower, high-performance network inside the broader insurance network and effective care coordination. This is a combination of administrative and clinical AI tools to identify the provider with the best mix of quality and price, and then engage with the patient to make the appointment.

Good patient engagement has additional benefits: engaged patients are 27% less likely to be readmitted to the hospital after discharge14, Medicare patients who adhere to medication protocols cost 27% less than those who do not adhere15; and patient engagement platforms can significantly reduce no-shows16. Each of these can reduce total cost of care or make providers more efficient. According to Olexa-Meadors, “Using AI to reduce system friction and frustration will make patients more proactive and truly engaged in their care journeys, take burden off of risk-bearing provider groups, and improve both outcomes and cost for everyone”.

Finally, one of the great (financial) benefits of administrative AI tools is that they free providers to see more patients. The Medscape 2023 Physician Compensation Report17 suggests that providers spend a total of 29% of their time on administrative paperwork. If a provider can eliminate nearly every administrative task a clinician performs to give them back 25% of their time you’d get 33% more clinician time. AI scribes, for example, can increase provider availability by up to 20%, which is enough to see 2-3 more patients per day18. That’s higher productivity by the physician and better leverage on the site of care, both of which we need in order to make VBC more financially compelling.

While tools like AI scribes can eliminate administrative tasks for clinicians today, AI ‘doctors’ should make this even easier. An AI doctor should be able to take its own notes, make a referral, write a script, submit a prior authorization, or address many of the other tasks a clinician is asked to perform.

These tools are not all ready today and many will take years before provider groups are comfortable deploying them, but many are already here or are close. Companies that build on the premise of the AI doctor and AI-enabled practice will be the winners. They’ll be the ones to figure out the best patient-AI interface, the best human doctor-to-AI doctor interface, the best contracts with payers, the best malpractice framework, and a host of other challenges that need to be solved.

So here’s the conclusion I’ve reached after all my analysis:

VBC in its incarnation from a decade ago is no longer a compelling venture investment - it’s too capital intensive and you cannot reduce MLRs sufficiently to create enough savings to justify the investment in VBC over FFS. It does, however, provide the payment model that rewards healthcare providers for using AI tools to reduce costs and improve quality. For that reason, I foresee VBC companies being the fastest to adopt new AI tools. The combination of AI tools and value-based payment models is a compelling investment and is a model capable of finally addressing the healthcare cost burden in the U.S.

1https://www.cms.gov/priorities/innovation/innovation-models/medicare-demonstrations/medicare-physician-group-practice-demonstration 2https://medium.com/p/cd155c800e74 3https://www.sec.gov/Archives/edgar/data/1564406/000119312520305587/d817452ds1.htm#toc817452_16 4Note: I’m ignoring all of the alternative cases here, like Oxeon and TLSG sold secondary along the way or they didn’t invest capital because they received equity in exchange for services or the round size might have been smaller or bigger because the point is still applicable. If you have details though, I’d be happy to update the analysis. I’ve heard anecdotally that some investors made 15x+. That would make the investment more attractive than the 6.9x calculated above but, in my opinion, it’s still reasonable to ask whether a 15x as a best possible outcome justifies an investment given all the failure modes (e.g., market downturns, fundraising challenges, competition, scaling multi-site clinics, etc.) when compared to investing in a FFS company 5 Institute for Health Metrics and Evaluation: https://vizhub.healthdata.org/dex/usa 6 Institute for Health Metrics and Evaluation: https://vizhub.healthdata.org/dex/usa 7https://business.optum.com/en/insights/better-outcomes-value-based-care-versus-fee-for-service-medicare.html 8 https://assets.humana.com/is/content/humana/2088482_CM-2024-VBC_Report_11x8.5pdf-1 9 Institute for Health Metrics and Evaluation: https://vizhub.healthdata.org/dex/usa 10 https://www.bls.gov/productivity/ 11 https://www.medscape.com/sites/public/physician-comp/2024 12 https://www.ama-assn.org/system/files/2021-01/cf-history.pdf 13 https://healthcostinstitute.org/hcci-originals-dropdown/all-hcci-reports/hospital-price-transparency-1 14 https://pmc.ncbi.nlm.nih.gov/articles/PMC10941103/#:~:text=Results,for%20all%20but%20two%20hospitals. 15 https://digitalcommons.unmc.edu/cgi/viewcontent.cgi?article=1001&context=coph_mha_capstone#:~:text=Several%20studies%20have%20shown%20an,billions 16 https://www.prospyrmed.com/blog/post/how-automated-reminders-reduce-no-shows#:~:text=Automated%20reminders%20are%20a%20game,patients%20feeling%20more%20cared%20for. 17 https://www.medscape.com/slideshow/2023-compensation-overview-6016341#18 18 https://www.uchicagomedicine.org/forefront/research-and-discoveries-articles/study-examines-economics-of-medical-scribes

Want to support Second Opinion?

- 🌟Leave a review for the Second Opinion Podcast

- 📧 Share this email with other friends in the healthcare space!

- 📢 Become a sponsor

About the author

Christina Farr

Christina Farr is a healthcare writer and investor. Formerly at CNBC and Reuters, she covers digital health, startups, and policy, blending reporting with analysis and investing perspective to help leaders navigate healthcare’s evolving landscape.

New York City