Tech-Enabled Healthcare Services Will Be the Winners of the AI Era

Alyssa Jaffee is a Partner at 7wire Ventures, a venture capital firm focused on digital health companies that empower individuals to take an active role in managing their health.

In 2022, we published an original piece in defense of tech-enabled services, arguing that it will persist as the dominant business model in digital health. Now that we are fully in the AI era of healthcare – with use cases present across all facets of the industry, and with startups and venture capitalists alike trying to build enduring companies amidst the excitement – I continue to hold this belief, and will be doubling down. In fact, I foresee our original predictions, including tight bundling of software with services to enhance adoption, pushes to address the totality of a patient’s needs, and increases in margins and LTVs, accelerating in the face of AI enablement.

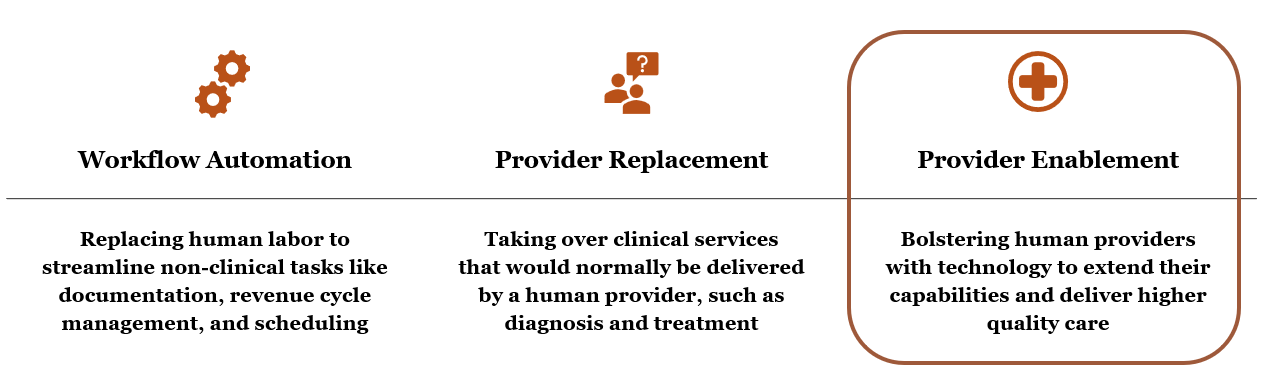

In health AI, we see a few primary strategies at work.

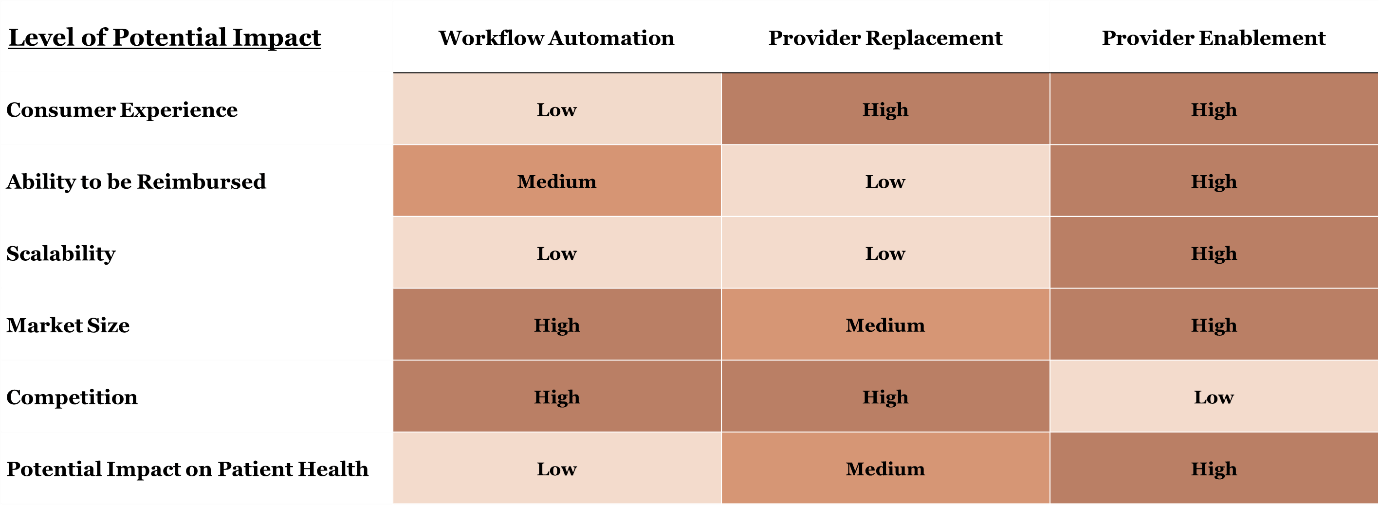

Workflow automation and provider replacement startups are building AI tools with an eye to selling them into health systems, payers, and life sciences organizations. Provider enablement or tech-enabled services startups already own the care delivery, and they will be using AI to make their own providers more efficient. VCs are already investing and will continue to invest more into the first bucket of tools. I will be investing in the latter, as I believe these companies continue to be positioned to win in the long run.

Allow me to make the argument. I’ll acknowledge here that I do have a bias in that my fund, 7wire Ventures, invests heavily in tech-enabled services (and openly acknowledges that this is our focus). But that very same bias gives me a first-hand perspective. I have seen many of these companies adapt to an AI era as they scale and find new efficiencies, so I’ll pepper in those anecdotes and case studies throughout.

Reserve Your Spot for Upcoming Webinars!

Webinar Topic | Panelists’ | Timing | Registration |

|---|---|---|---|

What will AI do for employer healthcare and benefits? | Nick Reber | May 19th, 2026 | |

Privacy AI and the future of HIPAA with the former founding director of ONC | Jodi Daniel, Christina Farr | June 3rd, 2026 | |

Not everyone can access the Top 1% of physicians. Will AI change that? | Daniel Stein | June 23rd, 2026 |

AI-native tech-enabled services companies will experience major lifts from the perspective of their unit economics. As these startups lean into more AI use – for example, scribes to reduce the time spent writing notes, AI-generated treatment plans, or patient engagement tools that help draft personalized messages to each member – they will be able to reach very different margin profiles. NOCD, which is a platform for complex psychiatric conditions where I sit on the board, has been able to use its internal AI platform to save their therapists two to twelve hours each week on administrative tasks like scheduling and drafting notes. In a 40-hour work week, this is extremely valuable. Not only does this free up time that therapists can instead spend in clinical sessions by upwards of five additional hours each week, but it focuses therapist time where it matters most. As a result, NOCD has seen improved per-therapist revenue, driving a more favorable economic profile. This is particularly important given the finite pool of providers.

There’s also a big opportunity here to transform care without waiting for a three-year sales cycle and implementation process. It’s my view that tech-enabled services businesses will be able to drive better clinical outcomes and, therefore, push payers to secure more favorable rates over time. One company we know used AI to create a “digital twin” of both the provider and the patient, which was then integrated into its clinical training process. This approach significantly reduced the cost of training while, more importantly, helping providers deliver higher-quality care and achieve better outcomes. With stronger outcome data in hand, the company was able to go back to payers and more than double its reimbursement rates. In practice, this translated into a dramatic increase in revenue per visit with top-line increases of over 200%.

Another area where the financials will meaningfully improve is operating expenses, as fewer team members will be hired at scale. Companies that are able to achieve greater care team productivity will reduce the direct cost of delivering this care. Tech-enabled services businesses will always need a supply of providers, but making those providers and care team members more efficient can create a meaningful lift on margin and cash burn. For instance, Transcarent – another one of my portfolio companies – helps employees navigate and access their care benefits, and the company has been leaning on AI to improve the member experience and reduce the burden that historically fell to care team members. As a result of their WayFinding AI platform, 83% of member questions are resolved without needing human intervention, allowing the Care Support team to prioritize their time on more complex needs. In addition, AI is driving improvements in care team capacity – with AI, preparing for a second medical opinion now takes eight to twelve minutes instead of the eight to twelve hours it used to take, allowing providers to see more members.

As tech-enabled services companies scale, we expect further cost savings across functions such as revenue cycle, back-office operations, training, recruitment, patient triage, and data analytics, as organizations increasingly leverage AI to automate workflows and reduce reliance on human labor. 9amHealth, a portfolio company that delivers cardiometabolic care, offers AI-extracted lab values, triage and routing, automatically drafted progress notes, and AI-generated member follow-up messages. As a result of these automations, they estimate a 11.3% uplift in gross profit driven by the equivalent of 14.2 FTE of care-team hours saved per month. The AI solutions used by tech-enabled services companies are often workflow automation tools, but by pairing them with human providers, these companies can deliver more outsized and differentiated value.

The Healthcare AI Paradox

There are high barriers to entry for building a care delivery business and partnering with large incumbent organizations (e.g., building out a clinical model, getting in-network with payers). As a result, while many startups may emerge in a category, the number that ultimately scale with enterprise customers is typically small. Health plans and employers rarely contract with dozens of vendors addressing the same condition. In areas like GI care, for example, a plan is unlikely to work with 20 solutions and instead will partner with only a small handful that demonstrate strong outcomes and operational reliability.

In contrast, for workflow automation and provider replacement solutions, incumbent customers may be choosing among a large range of solutions and struggling to figure out how these solutions fit within their existing workflows and systems. Implementation timelines, procurement requirements, compliance reviews, and long enterprise sales cycles can further slow adoption. Even when the technology works, many healthcare organizations lack the operational infrastructure to implement it effectively. As a result, many SaaS companies ultimately find themselves building service layers to ensure their insights actually translate into action. We saw this dynamic play out in areas like remote patient monitoring and chronic care management, where several startups claiming to be solely technology-focused ultimately had to build their own care teams because the provider organizations adopting the software didn’t have the operational capacity to act on the data. These dynamics help explain why pilot activity is high but scaled deployment remains limited, with only 3 out of every 10 AI pilots ultimately rolling out across an organization.

In healthcare, whether we like it or not, often the “keys to the kingdom” are held with the payers. Payers cover 73% of total health spending in the U.S., which makes their influence unparalleled. In order to build a massive company within healthcare, founders need to successfully unlock these incumbent dollars. Tech-enabled services companies are the ones best able to tap into this pool. And progress can happen rapidly once a business is embedded with incumbents – I’ve seen one example of a company that took three years to hit $1M in ARR, but then went from $1M to $10M in ARR the following year and $10M to $50M in ARR the year after that. For tech-enabled services, this level of massive revenue growth can be driven by just a few new contracts signed and/or better expansion within existing contracts. In addition, revenue is stickier after a contract is landed, leading to higher net dollar retention.

This means that the marginal opportunity for AI enablement is even greater for tech-enabled services businesses: if AI-enhanced care can lead to one additional contract, that represents massive incremental value for the business. Eventually, these companies will act as the virtual front door to healthcare, with AI tying everything together. Hybrid models, with both virtual and in-person interactions, will become the norm for insured patients to engage with our healthcare system.

For tech-enabled services companies, AI utilization is driving meaningful increases in valuation across both public and private markets. However, investors are giving credit just for the tangible outcomes that AI has already driven, not for the promise of future capabilities. Chrissy recently wrote about Talkspace’s sale to Universal Health Services and noted that investors only factored in minimal margin expansion, suggesting that the AI vision didn’t contribute to the valuation expectation. However, investors did believe in the business’s steady growth potential. Underlying this expectation are the revenue uplifts Talkspace’s use of AI have already driven – for example, when providers use AI insights in preparation for their clinical sessions, members are more likely to book additional sessions (i.e., higher LTV). We’ve seen a similar story play out for Hinge Health. The company has invested heavily into AI enablement, such as computer vision to track body movements and real-time feedback during therapy sessions. In 2025, as a result of their AI-forward platform, they reduced the number of human provider hours by 97% as compared to traditional physical therapy. This led to vastly improved unit economics, with the company reporting a GAAP gross margin of 80% in 2025. Unsurprisingly, they ended 2025 with an EV/Revenue multiple of 7.90, which is high for the industry average. On the other hand, for companies that haven’t yet fully figured out the best ways to leverage AI, the markets will likely be punitive.

In a venture landscape where many investors are investing in software over humans, we believe that there should be increased attention paid to tech-enabled services companies. Through a combination of direct impact on clinical outcomes, alignment with incumbent incentives, competitive defensibility, and elasticity to AI enablement, these companies are well-positioned to be the dominant winners. Investors should deploy more capital into these models. Meanwhile, founders continue to have significant amounts of white space within tech-enabled services. AI is enabling the next generation of these companies – with improved care delivery capabilities and economic profiles that were unattainable for prior generations of tech-enabled services companies – so now more than ever, it is time to build in this space.

About the Author Alyssa Jaffee

Alyssa Jaffee is a Partner at 7wire Ventures, a leading venture capital firm investing in digital health companies that empower individuals to become active stewards of their health. She currently holds board roles at NOCD, MedArrive, Brightline, Zerigo Health, Jasper Health, Summer Health, Transcarent, WellTheory, and the National Venture Capital Association (NVCA). She was named to Business Insider’s 30 Under 40 in Healthcare, Crain’s 40 Under 40, and Modern Healthcare 40 Under 40. She previously worked at Pritzker Group and co-founded TransparentCareer. Based in Chicago, Alyssa is a community-minded leader, mom of three, and advocate for equity in venture capital—with a passion for healthcare, mentoring, and bringing people together over shared meals.

Eric Shan is an Investor at 7wire Ventures, where he focuses on investments in digital health companies that empower the Informed Connected Health Consumer. Prior to joining 7wire, Eric trained at the Perelman School of Medicine at the University of Pennsylvania, where he also held roles in digital health and early-stage investing with firms including Flare Capital Partners, Springbank, Redpoint Ventures, and Rock Health Capital. He began his career as a Quantitative Researcher at Meta. Eric holds a BS in Economics from The Wharton School.

Want to support Second Opinion?

- 🌟 Leave a review for the Second Opinion Podcast

- 📧 Share this email with other friends in the healthcare space!

- 💵 Become a paid subscriber!

- 📢 Become a sponsor

About the author