The biggest winners from the Hinge IPO - and what that says about digital health investing

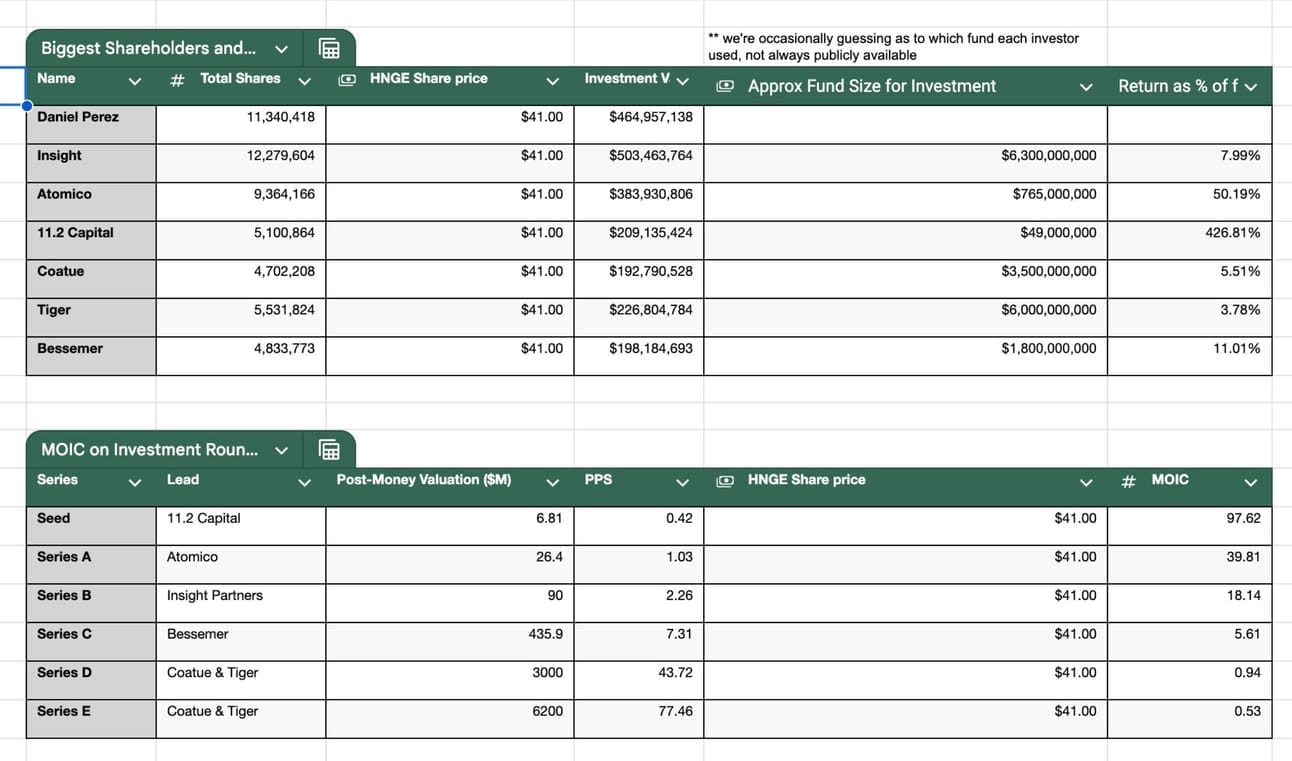

The biggest winners from the Hinge IPO? Well, according to Second Opinion’s analysis, it’s unsurprisingly CEO and co-founder Daniel Perez, whose stake in the business is worth more than $400 million.

And who else? Investors up to Series C did well. But one firm truly knocked it out of the park: 11.2 Capital. That represents a huge win for a female-led Fund 1 with a small AUM and a thesis to bet on emerging technologies including climate tech and health-tech. 11.2 should not be confused with the Chicago-based venture studio with a similar name.

11.2 Capital made its first bet on Hinge at the seed stage, investing out of a $49 million fund led by managing partner Shelley Zhuang. At the time, Yizhen Dong—now a growth equity investor at Koch Disruptive Technologies—served as a principal at the firm. So it was a team of two people that sourced Hinge Health and did the deal.

It appears that 11.2 Capital owns a roughly $200 million stake in Hinge, and its already brought in more than $25 million by selling shares at the IPO. It owns a little more than 5% of the business. Its multiple on invested capital or MOIC? An absolute monster. Paid subscribers can check out our deeper financial analysis and estimates below.

Also notable about 11.2: This small Fund 1 spotted a winner and just kept doubling down, which is the way to do it. 11.2 invested in the seed round in 2016 as part of a $2 million raise (remember when seed rounds use to be this tiny?), and in the $10 million Series A, per Pitchbook. The company continued to invest again in 2020 when Hinge raised a much larger round of $90 million and brought in bigger and more well-known VCs, like Bessemer and Insight. This fund kept following on every chance it could to protect its ownership.

Since the initial Hinge investment, Shelley continues to run 11.2 Capital, per her LinkedIn. And she also runs a new firm called Cannage Capital with Jacob Smith. According to a recent update, she brought her mom to the ringing of the bell for Hinge Health’s IPO.

Here’s the first key takeaway from the Hinge IPO for digital health investors - but with a caveat:

Small funds with modest AUMs can do extremely well in health-tech, but especially when they’re big enough to back their stand out companies and retain a strong ownership position over successive rounds. It’s very important to keep backing winners. Although that’s easier said than done. Hinge may not have been an obvious IPO candidate at the series A or B, and certainly not at the seed.

But also, there’s conventional VC wisdom that indicates 11.2 made a very gutsy decision that many small funds would not have, in favor of diversification. They took an extremely concentrated position into Hinge, given the size of the fund. If it had not paid off as well as it did, that would have been an extremely risky move. Thankfully for them and their LPs, it paid off.

Fund size matters more than you might think, as Health Velocity’s Saurabh Bhansali covered in a prior Second Opinion. It was still a strong return for Atomico, a European fund with a much larger AUM. And a good one for Insight and Bessemer.

These larger growth firms still did extremely well. These are also generalist firms, so it’s a win for the health-tech teams that may be presenting deals alongside investors that look at hotter areas like AI, cybersecurity, and enterprise software. Bessemer’s returns may be more moderate and just cleared growth targets, but relative to the vintage it’s a big deal. There are so few growth success stories in this vintage.

The last round’s investors did not fare quite so well, including Coatue and Tiger. In retrospect, a $6 billion valuation seems like a product of a very hot market and low interest rates. Hindsight is also 20/20. A lot has changed in the market in the past 3 years. Unfortunately, health-tech does not have many companies worth more than $10 billion, so it’s not an easy sector for growth stage VCs that need these returns in a shorter time frame.

And yet, our industry probably still needs the Tiger’s of the world. Without that, the early stage funds can’t get their big wins. Someone has to do that pre IPO round and invest tens of millions of dollars to fuel a company to an IPO, particularly when they’re not super profitable. If these firms don’t come in, future generations of digital health companies will need to generate Hinge-like exits while being far less private capital intensive.

Our view on this is that if valuations had been more modest, the later stage investors might have still done extremely well. But Hinge benefited from the big pop around Livongo, post its $18.5 billion sale to Teladoc. The growth stage investors we talk to regularly are still struggling to deploy capital for this very reason. There’s still companies out there that got overcapitalized at a valuation that was too high in the peak pandemic years, and it would require a lot of structure to make a return.

This is why we’re so excited about the early-stage businesses that are raising today. With right sized valuations - outside of AI - there’s a real opportunity for the entire cap table and founding team to get a strong return in health-tech. This is absolutely the wrong moment for investors to turn away from the category just as valuations are normalizing, and companies continue to be high-quality. The bets we’re making right now will finally reset the table.

Let’s talk about our second major insight by examining the winners and losers: Dilution for the founding team.

Hinge’s founders and early employees will have done well with this outcome. Hinge’s founders own far more of the company at exit than Omada’s founders. Omada is targeting a valuation of above $1 billion with its IPO.

Omada’s big owners include VC firms like Union Square Ventures, Revelation Partners, a16z, FMR, Cigna Ventures, Moon Growth Fund and Norwest. Interesting to note that Revelation Partners is a secondary liquidity-focused fund, a breed of fund which will become increasingly important as funds face limited exit options on some of their holdings. These investors all own significant chunks of Omada, relative to the founding team.

So why do Hinge’s founders own more? What can you chalk that up to? Hinge clearly raised at more optimistic moments, it’s a younger company, and it benefited from the post Livongo surge of hype around the space. Hinge got started in late 2014; Omada has been around since 2011. That is meaningful. Omada paved the way for more investment in the category by getting well-known investors to come in for the first time. It was very hard to get a digital health business off the ground in the early 2010s, and very few investors were eager to back these businesses.

Of course, it's not always fair to say “avoid dilution.” Founders do what they must to fundraise—especially in a market where structured, dilution-heavy term sheets are the norm. Without that capital, the business may not be able to continue with its growth trajectory. It might need to downsize, or even shut down. But perhaps it is worth nudging founders to consider the impact of dilution at every stage. We see plenty of examples of this, for instance, where founders had to give up a big stake in their business to venture studios or corporate VCs at the pre-seed. It’s not uncommon for us to hear from founders that they wished they had taken a moment to restructure the Cap Table and cram down those investors during subsequent rounds, in order to ensure sufficient skin in the game for the team.

VCs should also consider whether their founders - and the teams, including beyond the C-suite! - have enough equity to keep going until the exit, particularly given the long time horizons we see in health-tech.

And a final thought: Seed and Series A is where it’s at but we still need growth

Growth-stage investing in health-tech will be tough until valuations come down to mirror what we see in the public markets. But the good news is that it’s starting to happen.

Hinge generated liquidity for both individuals and funds. The investors at the seed and series A, B and C did particularly well. But it was not a huge success story for the investors who came in at the middle to late stages of the business. We need more companies to succeed in digital health and for the entire cap table to win, top to bottom.

If helpful to Second Opinion subs, here’s some approximations below based on best available data from Pitchbook, Google searches and the S1 filing. This is directional, particularly as it’s very hard to know which fund each of these firms invested out of. Some investments will come out of multiple funds. The MOIC is also too high for the earlier funds, because we don’t have clarity on exactly how much the earlier funds chose to top up in later rounds with higher valuations, like 11.2 and Bessemer. If anyone from those funds wants to reach out and correct the #s, we’re here for it.

Bottom line: We believe the companies forming today and in this vintage will result in the best returns in decades because firms are more valuation sensitive and companies are doing more with less. We also owe it to the Hinge’s of the world as that’ll boost investor appetite in the category, and also produce newly minted millionaires. Enter the era of the Hinge Health mafia!

Rebecca Mitchell, MD is the Managing Partner and CoFounder at Scrub Capital. She has built and led digital and virtual care products that reached 10s of millions of patients around the globe from start up through hypergrowth and IPO, while coaching teams on how to bring clinician expertise into tech companies and venture investing.

Interested in being a Second Opinion sponsor? Reach out for a media kit.

About the author

Christina Farr

Christina Farr is a healthcare writer and investor. Formerly at CNBC and Reuters, she covers digital health, startups, and policy, blending reporting with analysis and investing perspective to help leaders navigate healthcare’s evolving landscape.

New York City