Why digital health is about to enter a “scale game,” leading to more mergers

This is a co-written piece with 7wireVentures’s Alyssa Jaffee

The pandemic was a boom time for digital health. It created massive tailwinds as regulatory barriers were broken down, leading to more innovation than ever before. As the demand for virtual care skyrocketed, entrepreneurs were able to build virtual care companies without needing a physical location present in all 50 states. Enthusiasm for the sector amongst VCs also shot up in the wake a string of impressive exits: Livongo sold to Teladoc for $18.5 billion, and PillPack/ One Medical were acquired by Amazon for around $750 million / $2 billion respectively. Venture capital funding ballooned to more than $29 billion in 2021.

That hype period may have led to many positive developments for the sector, but also some new frictions. Money was flowing out the door so quickly that venture rounds were finalized without much diligence. We saw founders taking millions of dollars off the table in secondaries, and we saw news headline after headline announcing new rounds of capital sometimes a few months after the prior round had closed.

Somehow, amidst all the frenzy, the fundamental first rule of startups was forgotten: Focus on building a great company before all else. VCs investing at the time often found themselves looking at companies that Alyssa likes to call having more “sizzle than steak,” meaning the story was there but not the execution nor the operational excellence.

In the past few years, the market has changed, and there’s no denying it. Good companies are still raising capital, and we’ve seen more examples of that in the past few months. But investors are now far more disciplined on valuations (outside of AI), and on how much they invest. They want to see companies hitting their milestones and finding product/market fit. Because of this, we expect to see companies that struggle to prove a business model finding alternative exit paths or quietly shutting down in 2024 and 2025.

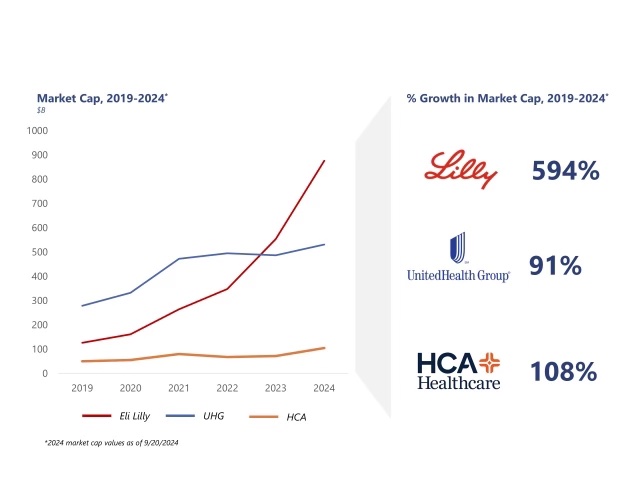

But here’s another trend that hasn’t gotten nearly so much attention. In the time frame that digital health has gone through its own hype cycle – both a boom and a bust – many of health care’s largest incumbents have been on a tear. In the 2020 to 2023 timeframe, as many publicly-traded digital health companies flatlined and struggled, companies like Eli Lily, United HealthGroup (UHG) and HCA continued to grow. To provide a specific example, UHG’s revenue in 2019 was $242 billion, and its market cap was $278 billion. By 2023, its revenue was up $372 billion for the year and its market cap shot up to $487 billion. By the time you’re reading this post, the company’s market cap has hit more than $531 billion!

Meanwhile, UHG’s Optum, announced revenue in 2019 of $113 billion. By 2023, its revenue was up to $227 billion.

So what does this mean for disruptors? Should they simply give up and let the big guys grow even larger?

Well, we’d argue no. But the game does need to be played differently. And to better understand that, we need to take a closer look at an acquisition that occurred in 2020 without a lot of fanfare. That acquisition truly benefited digital health as a sector, but we’d argue it would not have happened in 2024.

In 2024, the rules have been rewritten. So let’s take a walk down memory lane to understand what happened, what we can learn from it, and what’s changed in the years since.

Changing the playbook

Let’s take a look at a deal from four years ago: The $470 million buy-up of AbleTo by Optum.

Optum, which is a unit of UnitedHealth Group (UGH), acquired AbleTo to beef up its virtual behavioral health footprint. At the time, one would have to conservatively estimate that AbleTo was netting somewhere around $50 million in revenue and showing strong momentum. Those numbers were never publicly disclosed, so we can’t know for sure, although we have a hunch that this is about correct.

What’s important here is that Optum leaned in and paid attention when AbleTo was at that stage of growth. Why? Well, for the simple reason that very few companies with that revenue range have been acquired by incumbents in the years since. It’s not because these companies aren’t good acquisition targets, or that they couldn’t add something valuable strategically. Our theory is that because in the four years since the start of the pandemic, companies at a similar revenue run-rate as AbleTo are now simply too small to attract much notice.

In that timeframe, the incumbents have for the most part, gotten bigger as we discussed. So to make themselves acquirable, digital health companies also need to get bigger. Otherwise they’re just a drop in the bucket; too small to make much of a difference to any of these companies’ bottom lines.

So in light of that, we predict that in the next few years, we’ll see a string of mergers.

Digital health companies will join up to become bigger and better versions of themselves. As a result, they will likely become far more attractive to acquirers, particularly if the joint entity can bring together a strong network of providers with low churn; a seasoned executive team; competitive rates with payers; a brand that patients and consumers love; as well as a national footprint. It increases the probability by a lot to have more than $100 million in revenue, which is also where most companies need to be these days to IPO (at the floor).

Though, we will acknowledge here that these sorts of mergers may be harder in practice than in theory. Despite everything making sense on paper, merger decisions are a lot more than just integrated financials.

Most of these companies are venture-backed and have stakeholders with fiduciary responsibilities. There are co-CEOs in rare cases, but most companies will need to pick a de-facto leader, and not two. Mergers are not just combinations of contracts, but combinations of people and cultures – does the work ethic, value system and priorities align? And how do you get the two boards of directors to align?

And yet, we believe we’ll see a whole lot of mergers regardless because it provides an opportunity to achieve the kinds of exits companies are yearning for. And because investors will see it as a practical next step at a moment when capital required to grow is still hard to come by.

To conclude

The fact is that space could benefit from more exits to show the rest of the market how lucrative investing in digital health can be.

Digital health is a long game, we all know that. But many of our best and most experienced founders are still locked up in companies they started nearly 10 or 15 years ago, whereas in other sectors they might be on their second or even third venture. Exits are good for the space, because they show that there’s a light at the tunnel for investors, employees and founders, and they bring more enthusiasm to pre-seed and seed investors who don’t have much to go on when they write a check.

It’s also good for incumbents, because it helps them stay relevant and brings in new kinds of thinking into the mix. Incumbents only continue to succeed when they evolve and an acquisition injecting more digital health DNA could do that in spades.

Bottom line: U.S. health care is dominated by incumbents, but that doesn’t mean there’s no room for innovation. For founders in the space, it does mean making smart and strategic decisions to succeed, even if it means rewriting the playbook in real time. For those that end up making the decision to join up, we don’t doubt that two heads are better than one.

About the author

Christina Farr

Christina Farr is a healthcare writer and investor. Formerly at CNBC and Reuters, she covers digital health, startups, and policy, blending reporting with analysis and investing perspective to help leaders navigate healthcare’s evolving landscape.

New York City